Cover Victoria Allan, founder and director of Habitat Property in Hong Kong

Victoria Allan, founder and director of Habitat Property in Hong Kong

1 / 1

For our Money Milestones series, Victoria Allan of Habitat Property opens up about her investment deals, financial independence and involving her kids in her business

Buy, renovate, repeat. Over a few decades in property, this has become a familiar and successful pattern for Victoria Allan.

“It’s a really good way to save money because if you buy a property, you’re forced to pay the mortgage every month,” she says. “You’re forced to work harder because you have to make those commitments, so you create your own Catch-22 and are more driven to perform.”

Renovation costs are an added motivator and a creative outlet for Allan, who enjoys coming home from work at Hong Kong-based Habitat Property and poring over designs and finishes. So much so that when a project ends, she tends to feel lost. She’ll reward herself with a special purchase and then she’s off to scout the next opportunity.

“Everyone says property is location, but I focus on what’s different, whether it’s a unique view or outside space or the potential to combine and add value through renovation,” says Allan. “From an investment perspective, I’m quite aware of being female and think it’s important to be financially independent. If you can get assets together to add value through renovation, then you’re adding value for yourself long term.”

Below Allan shares lessons on putting deals together and building an innovative, flexible business—plus how to use property not only as an investment but also to enhance your lifestyle.

Don't miss: Women of Worth: A Series Celebrating and Supporting Financial Empowerment

Above Allan with the Habitat staff after a recent day of team-building activities (Photo: Habitat Property)

Allan with the Habitat staff after a recent day of team-building activities (Photo: Habitat Property)

1 / 1

Founded Habitat Property (2001) = closed first deal of HK$350,000

Growing up in Perth, Australia, we had family friends who were property developers. Before university, they sat me down and explained that real estate is a great career because you can travel with it and there are a lot of different things you can do in the industry. That’s proven to be quite good advice for me.

By the time I came to Hong Kong in 1997, I’d worked in valuation, planning, management, consultancy research and sales. I was transferred to the US for a year and when I returned in 2001, I decided to launch Habitat Property.

My first deal was for my ex-employer, a dot.com going bust, and I was negotiating out of a lease to terminate its commercial offices. The company was about to go into liquidation, so I was pushing for my payment. I knew which bank it worked with, and I opened an account there because it was the only way I’d get the money. If I had to wait a day for the cheque to clear, it’d be too late. I remember getting the cheque and running to cash it before 5pm.

That cheque gave me enough money for about six months during which I began working in residential leasing and sales. My first Habitat commission was a referral from a friend, and I earned about HK$80,000. Hong Kong is amazing in that people are very sweet and generous in supporting those starting businesses.

Don’t miss: What Does It Take to Become an Entrepreneur at 51? Josianne Robb Shares Her Money Milestones

The renovated Tung Fat building in Kennedy Town retains its classic curved exterior (Photo: Habitat Property)

1 / 4

First development project (2004) = structured HK$30 million deal

When I first saw the Tung Fat Building in Kennedy Town, I loved it and thought it’d be fun project. It was on the water with great views; the property could be renovated with elevators easily; and I knew there was a lack of quirky, loft-style apartments available. But I also went into it a bit naively.

The building came on the market after Sars, and it wasn’t very much: HK$7 million for the building except for two floors. I negotiated and put a deposit down without understanding that I couldn’t get financing. So suddenly I had a commitment to close but couldn’t get any bank loans because the building was old and I didn’t own it fully.

I brought in private investors through friends and clients, which meant I had to put a pitch together and structure a deal. At the last minute, an investor changed their mind to try to shaft me and force me to pull out of the deal so they could take it over. But I managed to borrow money off someone else and it all came in the day before closing.

Sweeping harbour views from one of the eight spacious apartments in the Tung Fat building (Photo: Habitat Property)

1 / 3

As we developed, we had to pay for everything in cash, so for years, I was taking money I earned from Habitat and putting it into this project. After we purchased the other two floors, we refinanced in 2009. We ultimately spent about HK$30 million among four investors to buy it all.

Over time, things went in our favour: the MTR went into Kennedy Town and the market kept going up. The first tenants came in early 2014, with the penthouse renting for about HK$115,000 and other units in the HK$80,000s and HK$90,000s. When we sold the building about three years ago, we were up nearly 10 times from the HK$30 million. It was an amazing, lucky turnaround.

Don’t miss: Inside Hong Kong’s Most Beautiful Revitalised Walk-Ups

Van Cleef & Arpels necklace (2004) = spent about HK$65,000

Every now and then I treat myself. When I finally put the whole Kennedy Town deal together and raised all the money, I went out to buy myself a little something as a commemoration: one of the Van Cleef & Arpels gold necklaces with a mother-of-pearl flower. It’s become my lucky necklace; I wear it if I need extra luck on a deal. As my mother always says, there’s no point working really hard and not spending some money on yourself. You’ve got to have a balance.

Allan combined two apartments to create this spacious interior overlooking the Sydney waterfront (Photo: Victoria Allan)

1 / 2

Sydney investment property (2006) = made a down payment of HK$758,000

In 2006, I had money from commissions that I wanted to invest and I decided to buy [a flat] in Sydney as I have friends there. Then I bought the apartment next door, bringing the total cost to AU$1.3 million (HK$7.58 million). I put 10 per cent down and set the architects from my Kennedy Town project to work combining the units. They knew my aesthetic, but we went way over budget and it took longer than we thought. It was super stressful financially for about a year and a half; I had to cut back on other costs. But then once it’s done, it’s done. If you’re looking at things over a 10-year horizon, then that’s okay. I’ve continued to rent or Airbnb the property.

When I buy property, I always try to add value. I’ve always found that if you start with something smaller, then you can sell up. Put that money to something else, sell that, and work your way up. Many people buy equities and shares or invest in other ways. I know property, and I think it’s a good asset class to always have some exposure to.

Don’t miss: Home Tour: An Art Deco-Inspired Sydney Home With Elegant Pink Rooms

Living and dining space in Allan’s Stanley home (Photo: Victoria Allan)

1 / 2

Home in Stanley (2008) = made a down payment of HK$16.8 million

I was renting in Mid-Levels with my then husband, and I must have showed this place in Stanley to about 50 clients; no one liked it. The more I came back and forth, driving clients from Central to Stanley, I thought, oh it’s not that far, and the more I looked at it, [the more] I liked it. It was small and really ugly but I saw the potential. I sold a property in Australia and part of a development project to put the money together, and the landlord gave me a six-month closing period. I put 40 per cent down on the HK$42 million cost (shortly before the requirement changed to 50 per cent) and took out a HK$5 million loan for renovations. It’s been great, I love living in Stanley.

Don’t miss: Neighbourhood Guide: What to Eat, Drink and Do in Stanley

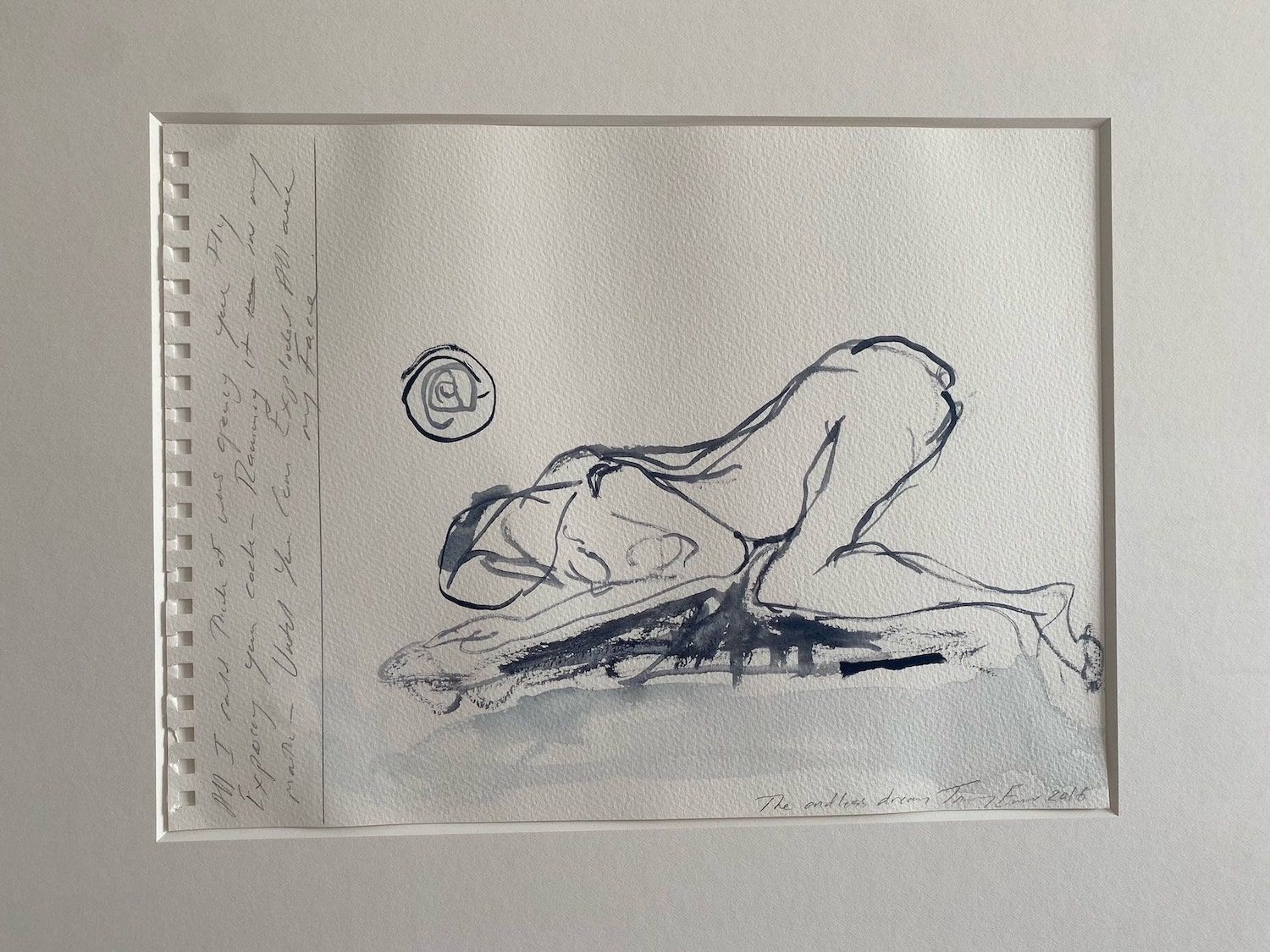

Above Work by English artist Tracey Emin (Photo: Victoria Allan)

Work by English artist Tracey Emin (Photo: Victoria Allan)

1 / 1

First work from her favourite artist (2018) = spent HK$200,000

This was a treat after we had sold the Kennedy Town project. The jewellery was the entry and the art was on the way out. I love Tracey Emin’s artwork; it’s amazing but also so expensive. This is a smaller piece that I really loved and it hangs in my bedroom, so I see it every day. It’s a nice reminder of the whole deal.

I say this to my team when they’re doing big sales: reward yourself, because it’s a lot of work. Women end up doing everything, right? You might be trying to get your business off the ground and dealing with kids’ activities and booking the holidays and sorting out things at home. I struggle with balance myself. It’s good to step back and do things for yourself or with your children.

Don’t miss: How I Work It: A Green Developer And Single Parent On Organising Her Work Life

Above Allan with her sons Rory, ten, and Gray, eight, in Ibiza, Spain (Photo: Victoria Allan)

Allan with her sons Rory, ten, and Gray, eight, in Ibiza, Spain (Photo: Victoria Allan)

1 / 1

Holiday home in Ibiza (2019) = spent just under HK$18 million

I’m very exposed to Hong Kong property, so recently I diversified by buying a home in Spain for nearly €2 million (HK$18 million), which is more of a personal lifestyle choice for me and my kids so that we have a base outside of Hong Kong. I think it’s important to set up property not just for investment, but also lifestyle, if you can. It’s a nice way to aim towards having a holiday home where you can spend time with family and friends.

You can do it through rentals, but it’s really expensive and doesn’t enable you to be there for very long. It made more sense to buy, renovate, use it ourselves and rent it out for the rest of the year to offset the majority of the costs. I got carried away and went over budget on renovation, but at the end of the day, I looked at it from an investment perspective: can I get my money back? And in markets like Ibiza, the rental yield is very strong.

Don't miss: What Can HK$12 Million Buy You Around The World?

Above Sunset view from Allan’s Ibiza home (Photo: Victoria Allan)

Sunset view from Allan’s Ibiza home (Photo: Victoria Allan)

1 / 1

Because you can’t go on holidays now with Covid-19, you end up working the whole time and everyone in Hong Kong is getting burnt out. So we decided to go to Ibiza this summer and deal with the quarantine. I felt that if I didn’t go away, I wouldn’t have any time off from work.

The house was just being finished, so I also needed to see it since I’d done the renovation all remotely—and I needed a break. We were in Ibiza for six weeks and we had lots of friends come to visit who we hadn’t seen for a while. It was wonderful. And now I have a refreshed view on work and being back in Hong Kong.

Loft-like interior of the Stanley office (Photo: Habitat Property)

1 / 2

New office in Stanley (2021) = invested in expanding the business

I’m very big on having the kids understand that I work, and the value of things, even if it’s hard in Hong Kong where helpers and drivers are common. Things aren’t free, and we have to be careful and watch the money. I make them come with me to look at properties and, with the Ibiza renovation, I involved them in looking at the plans so they could see what I do and the costs.

It also helps that they come by the office a lot. I opened a second office in June 2021 and chose Stanley because a lot of my team and a lot of our clients live in the south side. This office gives many of us the ability to work close to home part of the week. My kids can walk home from school and pop in to say hi, have a snack and do their homework. It’s nice for my team’s kids too.

We’ve hosted art exhibitions and talks in the space to engage the community around lifestyle topics related to real estate. It’s a really interesting time for the market, and we want to connect with a broader range of clients by doing something different from what’s typically done in Hong Kong in how we present property on our website and across social media. We’re trying to lead the way.

This article is sponsored by Citi Private Bank for our Money Milestones series, in which an accomplished woman reveals her financial thought process and the spending, borrowing and investing that reflects her growth. It’s part of Front & Female, Tatler’s platform to celebrate trailblazers and tackle timely, provocative issues through inspiring content and events. Join the community by subscribing to our newsletter and following #frontandfemale

About Citi Private Bank:

Citi Private Bank is dedicated to serving worldly and wealthy individuals and families, providing customised private banking across borders. With more than $600 billion in global assets under management, the franchise serves clients in over 100 countries. Citi Private Bank helps clients grow and preserve wealth, finance assets, make cash work harder, safeguard assets, preserve legacies, and serve family and family business needs. The firm offers clients products and services covering capital markets, managed investments, portfolio management, trust and estate planning, investment finance, banking and aircraft finance, as well as art and sports advisory and finance. Learn more

Topics

Kate is the regional editorial director of Tatler Asia’s Front & Female platform, which celebrates trailblazing women, breaks taboos, and tackles timely issues in Asia. She oversees the content, products, and community. A native New Yorker, Kate built up experience in travel and lifestyle coverage there before relocating to Hong Kong. She loves its urban-nature mashup and is pictured here blending in with her neighbourhood’s historic stone wall trees.